If you’re a UK-based SME looking for B2B payment solutions to manage incoming and outgoing cross-border payments, the following may sound familiar:

- High bank fees and FX costs are eating into your margins.

- Cross-border business payments are taking several days to clear in some cases. This can disrupt working capital, impact the customer experience, and potentially strain business relationships.

- Maintaining separate currency accounts with different banks (i.e. USD or EUR) makes reconciliation more complicated and drains a lot of time each month.

- Slow or inconsistent support means you’re struggling to resolve payment issues before they escalate.

Finding a B2B payment solution that addresses these issues isn’t straightforward. Different providers vary in cost, speed, currency coverage, and levels of support. To help you make an informed decision, this article covers:

- Signs it's time to switch away from your bank to a dedicated B2B payment solution

- The different types of B2B payment solutions for overseas payments

- How to choose the best B2B payment solution for your business

- Why IFX is a good fit for UK SMEs regularly making and receiving cross-border payments

- How a gambling company reduced payment disruptions and gained more control with IFX

Want to streamline your cross-border B2B payments? IFX can help. Book a call with us today.

When is it time to switch to a cross-border B2B payment solution?

Here are some key signs it might be time to switch away from your bank to a dedicated cross-border B2B payment solution:

Your payments are taking days to land, disrupting relationships and operations

Can your payments take days or weeks to clear, with no easy way of reaching out for support? Consistent disruptions could be a sign you need a solution that offers support allowing you to address issues faster (or avoid them altogether). You may also be left to search for answers in FAQs or via chatbots rather than being able to pick up the phone and talk to someone.

Your payment costs are high and unpredictable, cutting into your margins

Is your bank’s FX mark-up in the region of 2-5%? Do you find you’re being charged additional fees, such as transfer fees? If cross-border transactions are a key part of your business, you could be paying £1000s in additional charges per year.

On top of that, does your bank automatically convert incoming currency to GBP regardless of market conditions? If so, you could be losing out to unfavourable exchange rates.

You’re making multiple B2B payments one by one, draining time and resources

When paying contractors or suppliers overseas, do you have to log into separate online banking portals, create recipients, add payment details, and then make each payment individually? If your payment volumes are high, this could be taking days each month. It’s also prone to errors, which don’t get picked up until the payment is attempted, leading to further delays.

You're juggling several currency accounts, meaning complex reconciliation and a high risk of errors

Do you hold multiple foreign currency accounts with your bank? Do you have to log in to each account separately and top them up with the relevant currency before making payments? Does billing involve different IBANs for different invoices? If so, it’s time to find a solution that lets you manage all currencies in one place.

Different types of B2B payment solutions for cross-border payments

Not all cross-border B2B payment solutions deliver the same value or are suitable for SMEs.

Each option has its strengths, and your choice will depend on your payment volumes, the currencies you need, and the level of control and support you expect.

Here’s a breakdown of the most common cross-border B2B payment solutions:

-

Specialist cross-border payment solutions (like what IFX provides):

These providers offer efficient onboarding, competitive pricing, and multi-currency accounts with features purpose-built for small businesses.

-

Traditional banks:

Usually the first port of call for SMEs due to the convenience of existing setups. These are well-established and offer a full range of financial operations and merchant services, including expense cards and business credit cards. However, when it comes to cross-border payments, they can be slow, with “transactions often taking two to five business days to settle.” Banks can bake in “sneaky charges in inflated exchange rates and never tell their customers.” And, support is often limited, with SMEs “left to navigate impersonal call centres, clunky online portals, and long wait times.”

-

Mass-market fintech providers:

These are easy-to-access solutions with fast, app-based payment technology and wide currency coverage. However, being heavily automated, they tend to offer little support or transparency.

-

Open banking options:

These payment systems use digital payment APIs to facilitate direct bank transfers between accounts. They enable faster, cheaper payments, but coverage varies due to regional adoption and regulation. For example, “Open banking in Europe is 6–12 months behind the UK.”

-

FX brokers:

These specialise in currency exchange and can offer competitive rates, but they are designed mainly for large, one-off transfers.

Comparing different types of B2B payment solutions for cross-border payments

| Pros | Cons | When it makes sense | |

|---|---|---|---|

| Specialised cross-border payment solutions |

|

|

|

| Traditional banks |

|

|

|

| Mass market fintech providers |

|

|

|

| Open banking API providers |

|

|

|

| FX brokers |

|

|

|

How to choose the best cross-border B2B payment solution for your business

These five questions will help you identify the best cross-border B2B payment solution for your business:

1. How much support will I get when making payments

It's important to understand what level of support and control your provider offers when managing payments.

- Do they let you schedule payments to arrive on a set date?

- Do they let you choose the best route (SWIFT, SEPA, or Faster Payments) based on cost, speed, or destination?

- If additional information is required for the payment to go through, do they let you know in advance so nothing gets held up?

2. Can I manage all my international payments from one account?

Imagine you’re a UK company needing to make cross-border payments to the US, Europe, and Canada. Without a multi-currency account, you’re stuck moving money between banks, dealing with repeated conversions, and trying to reconcile balances across currencies. The right provider lets you handle all your payments from one account, saving time and simplifying your operations.

3. How easy is it to make bulk payments in different currencies?

It’s the end of the month, and your payment team needs to pay 150 contractors across seven countries. To avoid the headache of handling each payment one by one, does the provider have a bulk payment solution so you can make mass payments in minutes rather than days?

4. Can they help you keep your FX costs low and consistent?

If you process £100,000 in employee payments each month, do you know how much it’s likely to cost? And can you avoid unfavourable currency swings by locking in today’s rates for the next six months? The right provider will be able to give you a clear picture of your costs in advance and provide tools to mitigate currency fluctuation risk.

Why IFX is ideal for UK SMEs making regular cross-border business payments

We have over 20 years of experience helping UK SMEs optimise their cross-border payments. Here are some of the benefits you can expect by partnering with us:

Simplify your B2B payments via a single multi-currency account

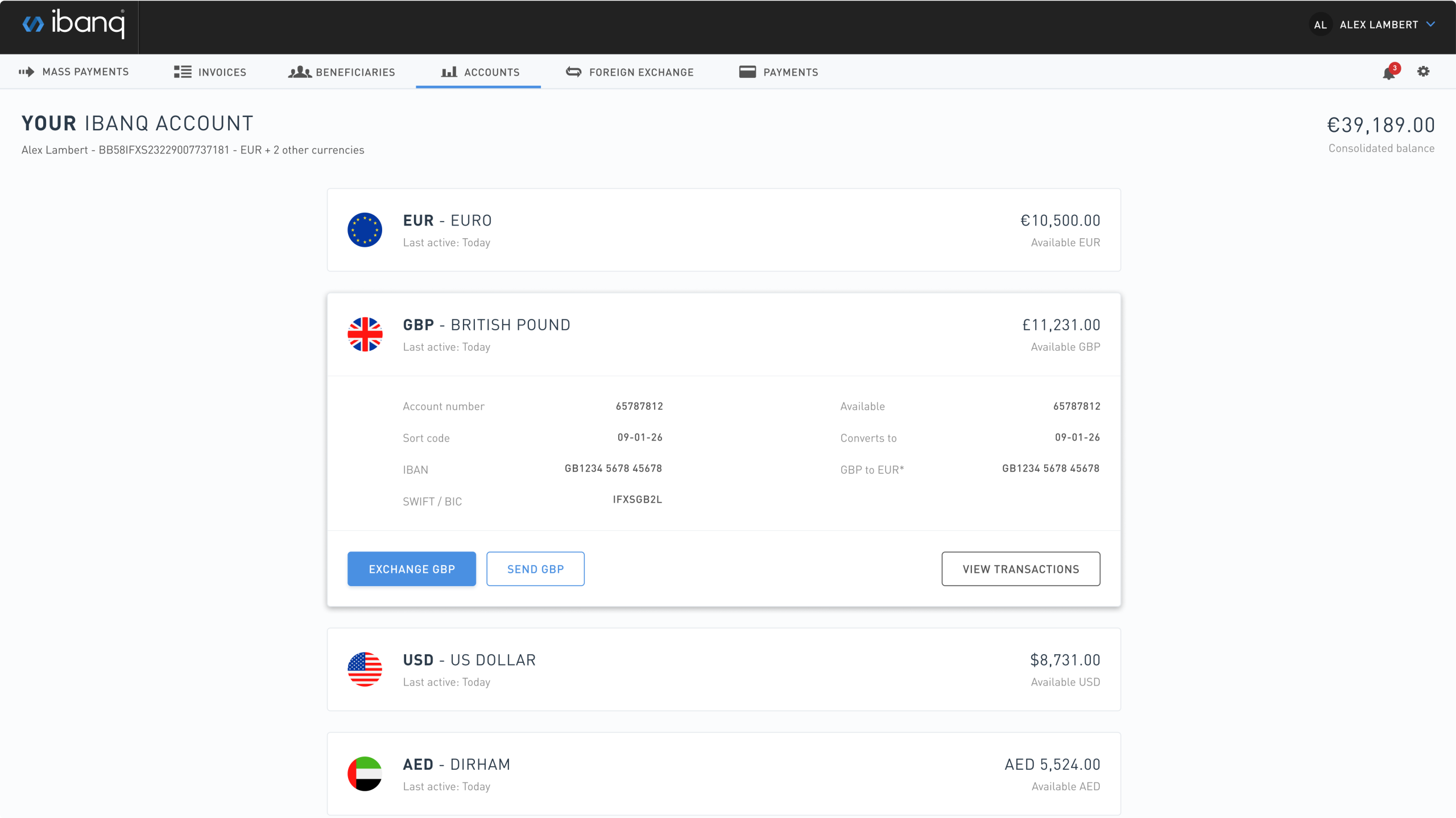

We provide a single multi-currency IBAN account to make mass payments in over 60 currencies and collect or hold funds in over 40. This gives you access to:

- Efficient onboarding: We aim to onboard clients as quickly as possible and provide a dedicated account manager to simplify the whole process.

- Reconciliation support and invoicing: With one IBAN for all currencies, invoicing is faster, with less risk of errors and reconciliation is much simpler.

- More efficient bulk payments: Through a single CSV upload, our Mass Payments solution lets you pay multiple payees in one go in 60+ currencies. The platform handles conversions automatically and performs CoP checks in advance, saving you time and reducing the risk of failed payments.

- As many as 1,000 sub-accounts: To manage payments in different regions or separate funds for specific reasons, you can open as many as 1,000 sub-accounts (each with its own unique virtual IBAN) under your main account. This allows you to segregate funds while retaining visibility over your company’s activity.

- Faster payments with multiple routing options: Choose the best payment route (SWIFT, SEPA, or Faster Payments) for each transaction, ensuring you avoid delays and unnecessary fees.

How a gambling company reduced payment disruptions and gained more control with IFX

Operating in a high-risk industry, a gambling company constantly saw payments lost or stopped for KYC checks. Faced with poor support, there was no clear way to resolve these issues, leaving the company exposed to ongoing disruption. The company also needed multiple virtual IBANs to manage different brands and simplify reconciliation. Unfortunately, they didn’t have an obvious way to do this.

To simplify its payments, the company switched to IFX. We provided a multi-account setup with sub-accounts for each brand, making it simpler to manage operations. The company also gained dedicated, service-led support. From the initial sales call onward, any queries would be handled by a dedicated account manager, ensuring accessible support. Whether asking about a lost payment or issue with their account, help would always be a phone call, email, or message away.

Work with a provider that simplifies every aspect of your payments

With the right B2B payment solution, your cross-border payments can be faster, more cost-effective, and more reliable. A specialised provider like IFX has the tools to make this possible, such as multi-currency IBANs and bulk payments.

Just as important is how they work with you. The right provider acts as a partnership, ensuring your payments run as intended while supporting you with responsive, personalised service. So, you can spend less time managing cross-border payments and more time expanding your business.

If you’re an SME after simpler, more efficient business payments, IFX can help with a tailored solution. Book a call with us today.

FAQs: B2B payment solutions

What is a B2B payment solution?

A B2B payment solution can mean one of two things:

- A tool (like the one provided by IFX) for managing payments between businesses. It’s used by finance or operations teams to send, receive, and reconcile payments. It’s often built for handling complex flows like payroll, supplier payments, or multi-currency transactions across borders.

- A checkout or payment gateway (like Stripe) built for businesses and usually embedded into platforms or marketplaces. These enable secure online payments (for example, in the case of wholesale ecommerce or procurement portals). The experience feels more like a consumer checkout, but the mechanics are built for business needs like invoicing, payment terms, and bulk orders.

How do I know if my business needs a B2B payment solution?

You might need a B2B payment solution if you regularly pay international suppliers, contractors and vendors, struggle with high bank fees, or spend time reconciling multiple accounts. A B2B payment solution can help make your operations faster, cheaper, and easier to manage.

Can B2B payment solutions handle bulk payments?

It depends. Banks and brokers typically don’t support bulk payments, but mass-market fintech, open banking, and specialised cross-border payment providers (like IFX) usually do support bulk payments.

The contents of this article do not constitute financial advice and are provided for general information purposes only. Links to third-party websites are included for convenience only, and IFX Payments holds no responsibility for the content, services, products, or materials on those sites. All testimonials, reviews, opinions or case studies presented on our website may not be indicative of all customers. Results may vary and customers agree to proceed at their own risk.