Businesses often use sub-accounts to alleviate the complexity of managing payments as they grow. Businesses with multiple international clients, subsidiaries, or internal functions often end up manually reconciling transactions across a patchwork of accounts. Each of these often come with differing restrictions and operating costs.

Sub-accounts offer a more structured and controlled approach. This article explains what they are, how they work, and which types of businesses benefit most from using them.

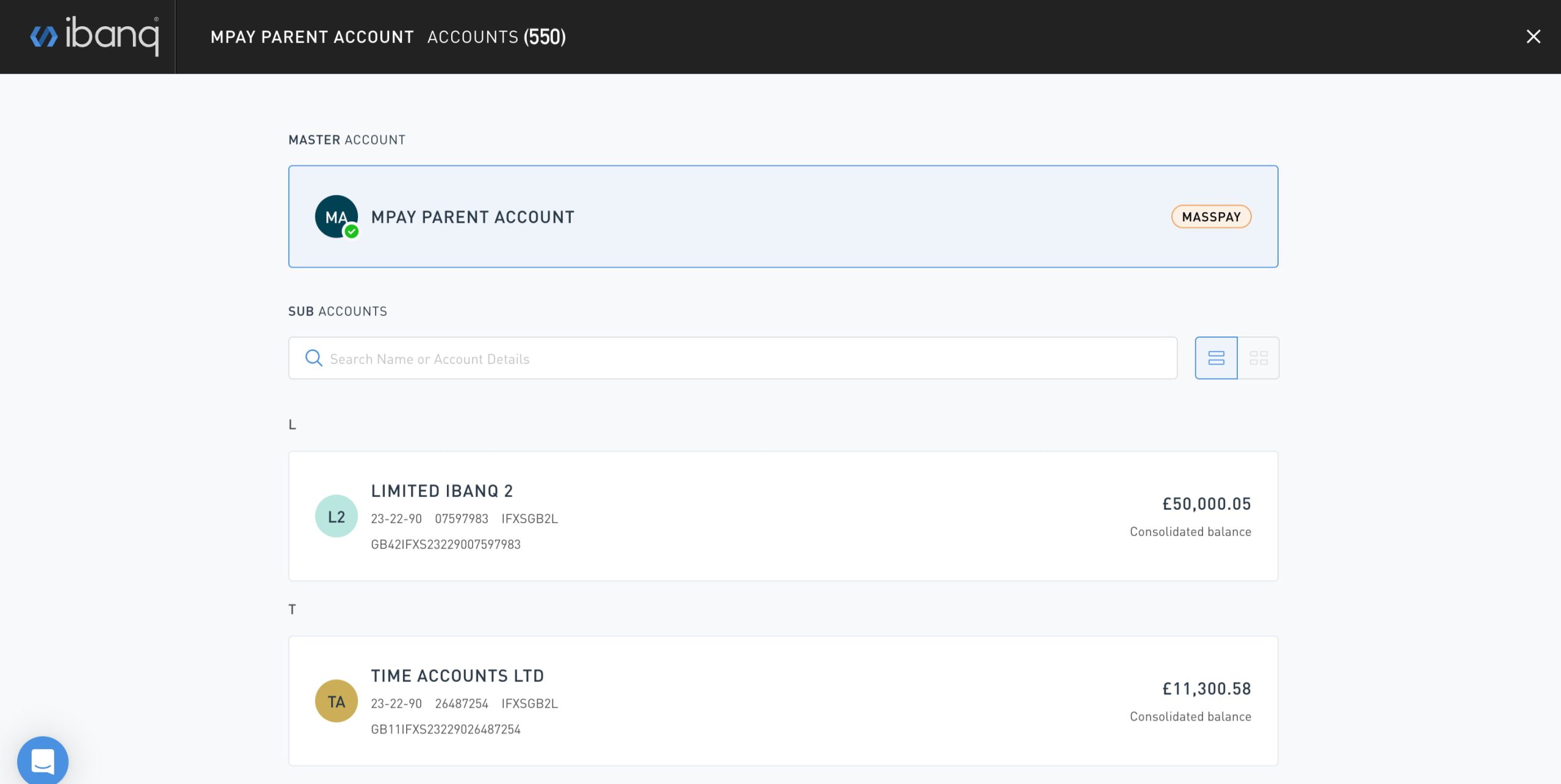

What are sub-accounts?

Sub-accounts are named virtual accounts that sit under a master account. People often refer to this structure as a parent/child relationship. Each sub-account has a unique virtual IBAN, which lets that sub-account send, receive and attribute funds.

From the perspective of the sender, payments arrive and leave as if they’re going to a distinct account. Unlike a traditional bank account, this account sits within a wider payment infrastructure that holds the funds.

Before we continue, here are a few key terms worth defining:

- Virtual IBAN – a unique account identifier assigned to a specific virtual account. It can receive payments just like a standard IBAN.

- Master account – the parent account from which sub-accounts are managed.

- Fund separation – the operational segregation of funds by entity, client or purpose within the account structure, for reconciliation and reporting purposes. Legal ownership of funds remains with the master account holder.

- Parent/Child Hierarchy – The organisational relationship between the Master Account and the sub-account. The Master Account holder (Parent) has oversight over the Sub-accounts (Children).

What sub-accounts are NOT?

It’s important to note that sub-accounts are not separate traditional bank accounts with their own independent interfaces. Each sub-account may need its own onboarding and approval, but the master account holder remains responsible for the underlying client. However, it’s significantly more efficient than applying to a new bank for every account.

The bottom line

Businesses with multiple sub-accounts gain the structural clarity of multiple accounts without the administrative overhead of maintaining them independently.

Why do businesses open sub-accounts?

The advantages come down to four core things: clearer fund separation, simpler reconciliation, consolidated oversight, and the ability to scale without restructuring.

Clearer fund separation

For businesses handling money from third parties, keeping funds clearly separated is an operational requirement. Sub-accounts make that separation more manageable, and less of a burdensome administrative task.

Some examples of where sub-accounts could be used are:

- Ring-fencing client balances.

- Isolating treasury from operational cash.

- Keeping different projects cleanly separated.

Simpler reconciliation

Because each sub-account has its own virtual IBAN, incoming payments are automatically attributable. The account structure significantly reduces the need to manually match transactions to a client or entity after the fact.

For finance teams managing high volumes of transactions across multiple entities, that’s a meaningful reduction in manual effort. A Gartner survey found “73% of accountants report that their workload has increased because of new regulations”.

Many will be looking for tools to perform back-office tasks more efficiently. Using sub-accounts should also reduce the risk of reconciliation errors. This is a common concern amongst accountants. The survey also found that 59% of accountants make several errors per month.

Real-time oversight at scale

Sub-accounts don’t mean losing sight of the bigger picture. Finance and operations teams can easily view individual balances and access statements for each sub-account. Firms can also apply transaction monitoring, restrictions, and reporting at a more granular level.

A structure that grows with the business

New sub-accounts can be added as the business evolves. That could be when onboarding a new client, entering a new market, or separating a new internal function. You don’t need to restructure your entire account setup each time. The infrastructure is already there.

Who uses sub-accounts? Key use cases by business type

They aren’t a one-size-fits-all tool, but they consistently work well for businesses operating at scale. Or those managing multiple payment flows. There is increasing demand for virtual accounts to assist with streamlining financial processes.

According to market analysis, the “Virtual Account software market [will] reach USD 3.5 Billion by 2033”. A Deloitte survey of CFOs found that “96% expect to see a rise in investment in digital technology and assets by UK companies over the next five years.” Here’s how different types of businesses put sub-accounts to work.

Payment Service Providers (PSPs) and other fintechs

This type of account can be used by PSPs to ring-fence client balances from their own operational funds.

Fintechs building their own payment platform can use sub-accounts – usually provisioned via API – to give users named, multi-currency accounts. That’s all without each of those users needing a direct banking relationship.

When PSPs or fintechs use sub-accounts to service underlying clients, they need the right controls in place. That means transparency over customers and payment flows, and safeguards against the risks of nested financial activity.

Example: A B2B payments fintech wants to give its merchant clients individual named accounts with their own IBANs, through its own platform. Using API-managed sub-accounts, it can create a virtual IBAN for each merchant. It can also show live balances in its interface.

Businesses with multiple subsidiaries

As groups grow across regions or brands, a single business account often stops being practical. Sub-accounts might help treasury teams, used to manually splitting and reconciling transactions, with limited visibility across subsidiaries.

They let each entity within a group have its own virtual IBAN, with funds clearly attributed and trackable. At the same time, the parent company can see all the individual balances – so group reporting is streamlined.

Example: A media group with production companies in the UK and the UAE sets up a sub-account for each entity. They can now track production budgets and revenue inflows independently. They can also give the group finance team visibility of balances without exporting data from three separate platforms.

Businesses operating across multiple jurisdictions

For collecting or paying out in multiple currencies, region based sub-accounts make cross-border operations easier to manage. Use cases might include international payroll, supplier payments, or receiving revenue from different markets.

Separation by territory has these potential benefits:

- Reduces the risk of unnecessary FX conversions.

- Makes local reporting easier due to holding balances in separate currencies.

- Gives treasury teams a clearer picture of currency exposure.

Of course, you should still consider local regulatory requirements, sanctions exposure, and other obligations when you structure sub-accounts.

Example: An international staffing company pays contractors in 20 different countries. It sets up sub-accounts for teams in different regions, using different currency balances in each one. Therefore, payments go out in the right currency, no conversion needed. The finance team can then reconcile by region rather than sift through a single blended transaction history.

Purpose-driven accounts: treasury, payroll, and operations

Sub-accounts are useful for internal structure too and go beyond client-facing use cases. A well-structured sub-account setup can handle all of the following without the overhead of multiple standalone accounts.

- Separating treasury reserves from day-to-day operational spending.

- Keeping payroll funds ring-fenced ahead of payment runs.

- Isolating capital allocated to a specific project.

What to look for in a sub-account provider

Not all virtual-account offerings are built the same. If you’re evaluating providers, here are the things that matter:

- Multi-currency capability. If your business operates across currencies, your sub-accounts need to as well. Check which currencies you can hold and transact in, and how broad the currency coverage is. Is it just 5 or 6 major currencies or can you access more currencies than this?

- Payment rail access. Does the provider support the rails you need, e.g. Faster Payments, SEPA, and SWIFT? The right combination depends on where your payments are going and how quickly you want them to arrive.

- API access. For PSPs and fintechs, the ability to provision and manage sub-accounts through their own tech stack is essential. Look for a provider with a well-documented API that supports the workflows you need.

- Regulated infrastructure. Sub-accounts should sit within a fully regulated payment account structure. Understand how client funds are handled and what protections are in place.

- Onboarding support. If you’re a PSP managing sub-accounts for clients, it’s important to understand sub-account onboarding. A provider with experience in complex business profiles will make that process considerably smoother.

Sub-accounts with IFX Payments

IFX Payments offers sub-accounts as part of its ibanq multi-currency platform. Each sub-account comes with its own virtual IBAN and access to the full platform infrastructure. This includes:

- Balances in over 40 currencies.

- Support for Faster Payments, SEPA, and SWIFT rails.

- FX execution.

- Individual and consolidated balance views.

- The master account owner can turn features on or off as requested.

We have 20 years of experience working with complex business profiles. We understand the challenges of servicing many clients or subsidiaries. That includes CSPs, PSPs, financial institutions, and multi-entity corporates. If your business has payment flows that traditional banks struggle to accommodate, we could be the right alternative.

Get in touch to find out if sub-accounts are the right fit for your business.

Frequently Asked Questions about Sub-Accounts

What is the difference between a sub-account and a bank account?

A bank account is a standalone account held directly with a bank, requiring its own application and onboarding. A sub-account is a virtual account that sits within an existing payment account infrastructure – typically provided by an e-money institution. It has its own virtual IBAN and can send and receive funds independently.

Can I open sub-accounts for my clients?

Yes, with the help of the sub-account provider who will onboard the underlying client. You, as the master account holder, will remain responsible for managing the underlying client. The provider (IFX in this case) will apply appropriate oversight controls. PSPs commonly use sub-accounts to give each of their clients a distinct virtual IBAN within a single platform.

Do sub-accounts have their own IBANs?

Each sub-account has a unique virtual IBAN. It can receive payments on its own. This makes it easy to assign funds to the right account or entity.

How many sub-accounts can I open?

The total number of sub-accounts can vary depending on the provider. Whilst there is usually no technical limit, for IFX Payments the number of sub-accounts is limited.

This depends on IFX Payments risk appetite, financial crime controls, and operational capacity.

It also requires initial approval and ongoing review. Nonetheless, should each sub-account comply with these parameters, scaling businesses and PSPs should have plenty of room to grow.

What businesses benefit most from subsidiary accounts?

Businesses with multiple payment flows tend to get the most from sub-accounts. That includes:

- PSPs and fintechs.

- Multi-entity corporate groups.

- Businesses operating across several currencies or jurisdictions.

Any organisation that needs to separate funds by purpose – such as treasury, payroll, or project-specific accounts.

The contents of this article do not constitute financial advice and are provided for general information purposes only. Links to third-party websites are included for convenience only, and IFX Payments holds no responsibility for the content, services, products, or materials on those sites.